Ooredoo Mobile Money

Building and scaling a consumer wallet for Qatar's migrant workforce — from regulatory approval through to $4bn+ in annual transaction flows.

The challenge

Qatar's workforce is overwhelmingly migrant — millions of workers, most unbanked, paid in cash and sending money home to families across South and Southeast Asia. Payday meant queues, cash-handling risk and remittance costs that took a real bite out of already modest wages.

The opportunity was clear but the execution was hard: a mobile wallet serving customers the banks didn't want, in a heavily regulated market, needing central bank approval, banking partners, international remittance rails and an experience that worked for users across many languages and literacy levels.

Scope — was this real?

The demand was visible on every street on payday — but visible demand isn't a business. We pressure-tested the market size, the unit economics of low-value high-frequency transactions and critically, the regulatory path: what would the Qatar Central Bank approve, under what conditions and with which banking partners standing behind the funds?

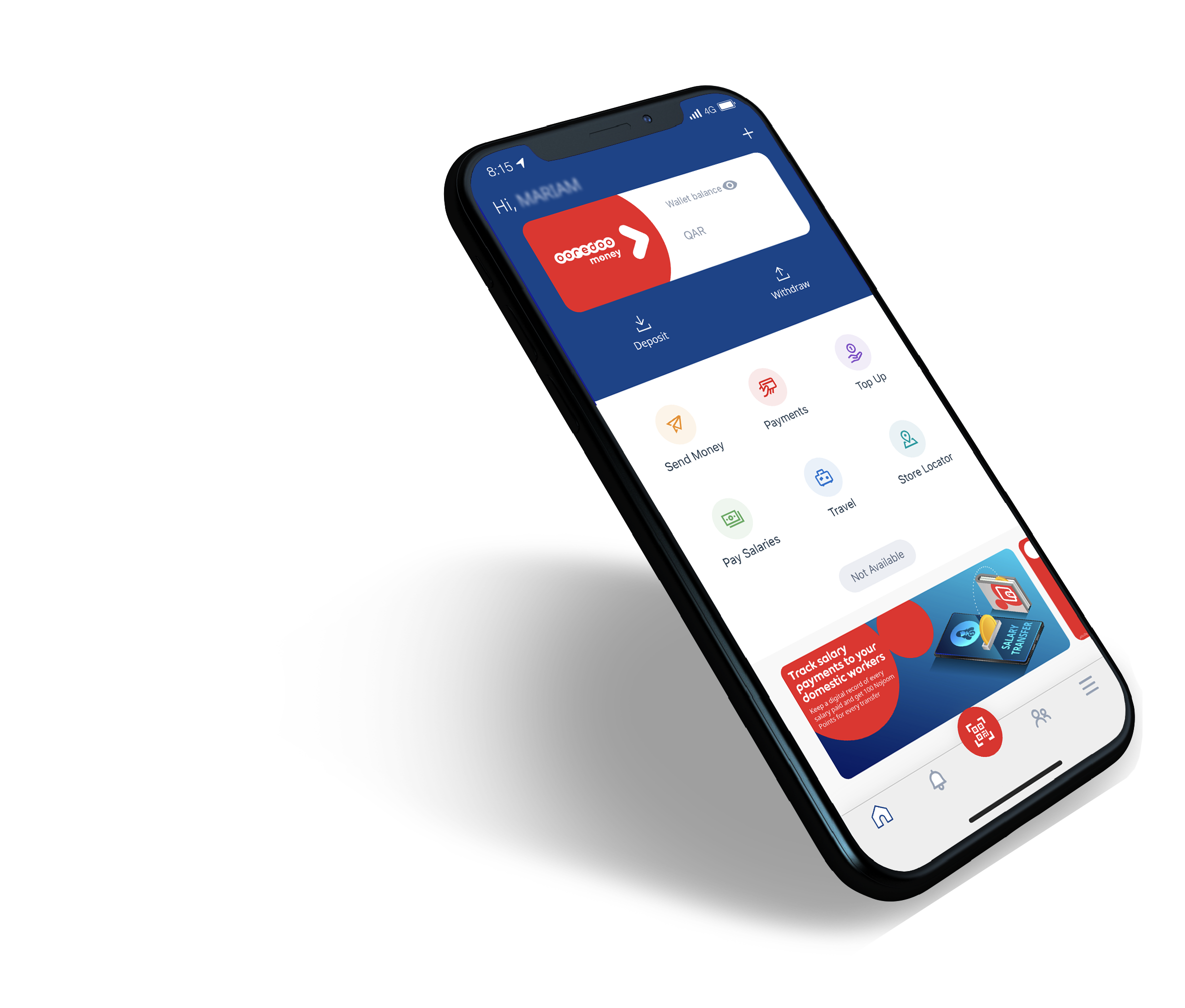

Shape — the product and the rails

We shaped the wallet around the jobs that mattered most to the customer: receive salary, send money home, pay bills, buy airtime. The rails came together as a partner stack — QNB holding the banking relationship, Mastercard on cards, SAP and Wipro on the platform and compliance build, MoneyGram for international remittance corridors.

The experience was designed for the real customer base: multiple languages, simple flows and agent-assisted onboarding for customers who had never used a financial product before.

Solve — build, launch, govern

The platform was built, integrated with the partner stack and taken through central bank approval to a live launch. Salary disbursement came first — getting employers to pay wages directly into wallets solved distribution and gave customers an immediate reason to activate.

From there the service layers were added in sequence: P2P transfers, bill payment, airtime, international remittance through MoneyGram and a co-branded card programme with Mastercard.

Scale — growth that held

Each new service was piloted, refined, then rolled out at scale. Salary volumes brought predictable monthly float; remittance and bill payment turned that float into transaction revenue; the card programme extended the wallet into everyday spending.

The compliance and operations grew with the volumes — the controls that satisfied the Central Bank at launch still held as the wallet processed billions of dollars a year.

Live product: Ooredoo Mobile Money + MoneyGram international remittance

Scaled beyond expectations

$4bn+

in annual transactions through the wallet by 2016

$250m+

annual revenue by 2017

250k+

users — over 40% of the addressable market

5

new services: P2P, bill payment, salary transfer, international remittance and a co-branded card

Building something like this?

Wallets, cards, remittance, regulated launches — this is the work I do. Tell me what you're facing and I'll tell you honestly whether I can help.